India’s ₹2 Lakh Crore Locked Savings Crisis: How KYC Overreach Is Failing Account Holders

· Free Press Journal

Financial regulators are guided by a simple mandate: protect depositors, policyholders, and investors. The RBI, SEBI, and IRDAI have steadily tightened rules to safeguard the system. Yet, a paradox has taken root. In trying to protect financial assets and prevent money laundering, the system is increasingly making the assets inaccessible to their rightful owners.

Scale of the problem

Visit turconews.click for more information.

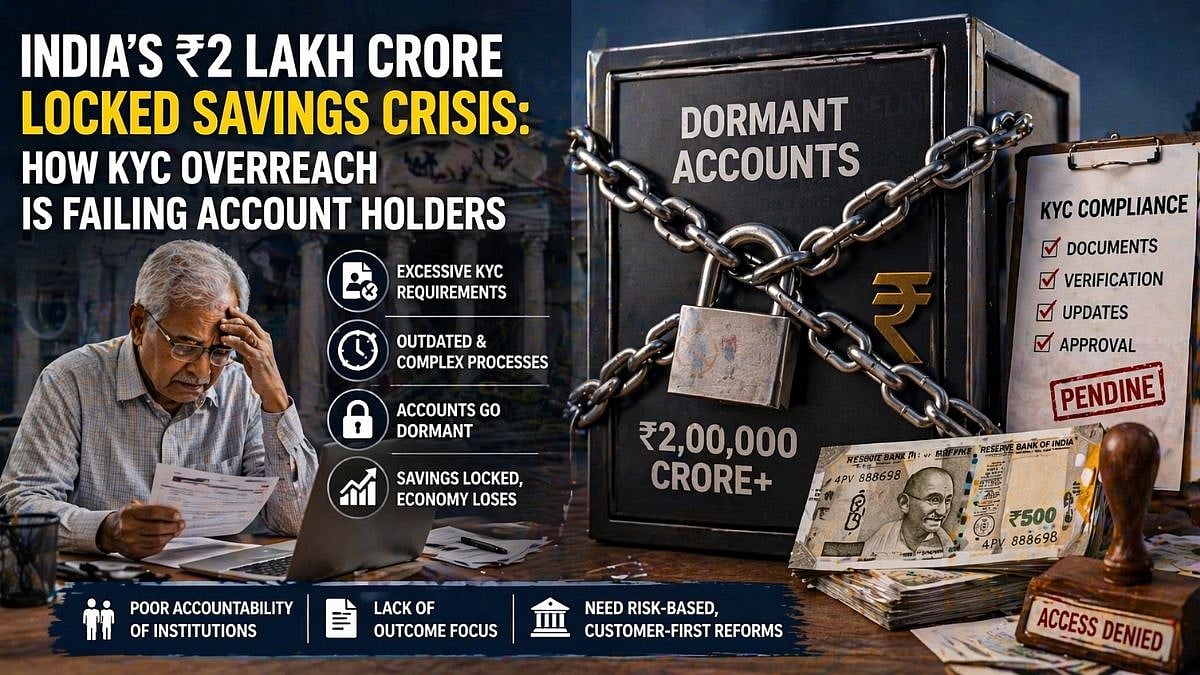

This is not a marginal inefficiency; it is a structural failure of regulatory design. India today has over Rs 2 lakh crore locked in dormant bank accounts, unclaimed insurance proceeds, idle mutual fund folios, and other financial instruments. But this headline number understates the problem. Beneath it lies a much larger pool of inactive accounts, funds that are neither used nor formally classified as unclaimed.

The KYC overload

The modern financial system runs on KYC norms designed to prevent money laundering and illicit activity. Over time, these norms have become more rigorous and more intrusive. That trajectory may be understandable. What is not is their indiscriminate application. A small savings account with a few thousand rupees is often subjected to the same procedural intensity as a high-risk account. This is not risk-based regulation; it is compliance maximalism.

In a country that has built a sophisticated digital identity stack with Aadhaar, PAN, tax records, and banking trails, KYC updation still routinely requires customers to fill forms, submit documents repeatedly, and navigate fragmented processes. Even where digital options exist, they are inconsistent. The system demands modern compliance through outdated processes.

There is also a more fundamental question that deserves examination. It should be found out whether any cases of significant money laundering can actually be attributed to the failure of KYC. The reality is that most large money laundering activities have historically taken place through fully KYC-compliant accounts. Yet, the burden of ever-tightening KYC falls not on such actors but on ordinary accounts such as widow pension accounts, senior citizen accounts, small startup accounts without compliance bandwidth, MNREGA-linked accounts, and others that have little or no connection to money-laundering risk.

Barriers instead of safeguards

For many, especially the elderly, migrants, or those less digitally fluent, this becomes a barrier rather than a safeguard. Accounts are first restricted, then rendered inoperative, and eventually classified as dormant. Recovery then becomes a procedural exercise rather than a simple interaction. The intent is compliance. The outcome is exclusion.

India attempted to solve duplication through centralised KYC. The cKYC was meant to create a single source of truth. Yet, customers continue to be asked for KYC updates by multiple institutions. The system shares data, but not responsibility. Each institution remains individually liable and, faced with regulatory risk, prefers to re-verify rather than rely on shared data. Centralisation without accountability reform has only multiplied friction.

From inactivity to economic loss

The problem deepens when one looks beyond dormancy to inactivity. Across the financial system, a vast volume of funds sits in inactive accounts with no transactions or engagement. These escape regulatory focus but are already economically disengaged. Money that should be spent or invested instead sits idle, earning little and contributing nothing to economic activity. Over time, it drifts into dormancy and eventually into unclaimed pools, such as those administered by the Investor Education and Protection Fund Authority. By then, recovery is difficult.

In a capital-scarce economy, this is a serious silent drag. It reduces the velocity of money, weakens consumption and investment, and locks household savings into low productivity.

Misaligned incentives and narrow accountability

Institutions have little incentive to fix this. Dormant and inactive accounts are cost centres. They require maintenance and compliance but generate no revenue. If the customer is unreachable, even basic charges cannot be recovered. The rational response is minimal compliance. The system is efficient at onboarding customers but indifferent to losing them.

This is reinforced by a narrow definition of accountability. Institutions are required to inform customers about KYC requirements. Once a notification is sent, the obligation is deemed fulfilled. Outcomes are not measured. If the customer does not respond, the account becomes dormant. If nominee details are missing and the account holder passes away, funds remain unclaimed. The institution has complied. The customer has failed. A system that measures success by notices sent rather than access ensured is not protecting customers; it is merely protecting itself.

The data gap

Compounding this is a lack of granular data. Regulators publish aggregate numbers of unclaimed assets, but there is little insight into causation. How much dormancy is driven by KYC friction, how much by missing nominees, and how much by other factors remains unclear. Without this understanding, responses remain generic. What is not measured is not managed.

Reassigning responsibility

The solution lies not in more rules, but in reassigning responsibility. Regulation must become risk-based, with lighter requirements for low-value accounts. KYC must shift from a customer-driven to a system-driven process, leveraging existing verified data. Institutions must be held accountable for outcomes, with dormant and inactive account ratios treated as supervisory indicators. Nominee registration should be universal by default.

Conclusion

When large volumes of money become inaccessible to rightful owners due to procedural flaws, when compliance replaces accountability, and when regulators mandate rigour but ignore outcomes, this is a huge regulatory failure.

India’s financial system has achieved scale but has normalised friction that distances people from their own money. Protection cannot come at the cost of access. Regulation cannot become an end in itself. The test is simple. Can people use their own money when they need it? For millions of accounts, the answer is uncertain. Until responsibility shifts from the customer to institutions, the system will continue to lock savings away, to the detriment of both citizens and the economy.

Today, this KYC “Bhasmasur” is the biggest regulatory failure of the last two decades.

The writer is a retired IRS officer and former Chief of Surveillance at SEBI, and an advisor to corporates, market participants, and tech entrepreneurs.